Loading content …

MIPIM 2024: More Realism and Cautious Optimism

The much anticipated MIPIM 2024 real estate event just wound up. Notwithstanding the bleak overall situation, sentiment among the real estate pros was cautiously optimistic. They have also adopted a largely realistic view on the subject of price corrections. After nearly two years, market operators have adjusted to the new parameters and have begun to engage in market activities again, albeit at a moderate pace. There has also been a slight increase in transactions and financing arrangements – although it started from a low level. While the crisis has yet to be overcome, we are facing the remainder of 2024 with a tad more confidence after this year’s edition of MIPIM.

Signs of optimism emanated not just from MIPIM. As a look at the recently published BF-Quartalsbarometer Q1 2024 reveals, real estate lenders are also suggesting that the strain has begun to ease. The inflation rate in Germany is declining, albeit slower than had been expected. It has not yet dropped back into the ECB’s target corridor of 2 percent. Last month, the inflation rate stood at 2.5 percent. The central bank’s response was therefore marked by caution. Interest rate cuts are not to be expected in the near term (yet). Still, one of the most frequently discussed questions in Cannes was whether and, if so, how far the interest levels could actually come down during the second half of the year.

According to the Quartalsbarometer survey, financiers are generally more optimistic than they were by the end of last year. The budding optimism is mainly attributable to two drivers. On the one hand, the steady downtrend of the inflation demonstrates the effectiveness of the ECB interest rate policy. This inspires reasonable hopes for interest rate cuts in the longer term. On the other hand, there is no evidence that market trading has ceased altogether. Despite the high level of building finance rates—when compared to the past decade—the volume of new lendings is visibly growing. As interest rates of about 4 percent for end customers coincide with softened prices, the number of loan signings is back on the rise. Especially financing for residential real estate has been approved more often than it used to. However, a closer look at the barometer’s hand is in order. Even after having moved up a notch, it remains deep within the red range. The consequence is a persistently restrictive lending practice. Despite the modest recovery, it would therefore be premature to speak of an end to the crisis.

Aside from property developers, the strained market situation continues to present challenges to property asset holders. Refinancing existing properties has proven difficult and time-consuming. Especially commercial real estate is closely scrutinised for impending capex requirements and demonstrable potential for alternative use. Market players are increasingly worried to end up with stranded assets in their portfolios. This is reflected in significant mark-downs of mortgage lending values and growing margins. The due diligences that comes with (re-)financing requests have become more extensive and therefore take longer. With that in mind, property asset holders should start talking to financiers as early as possible lest they run out of time.

Interest Rate Development

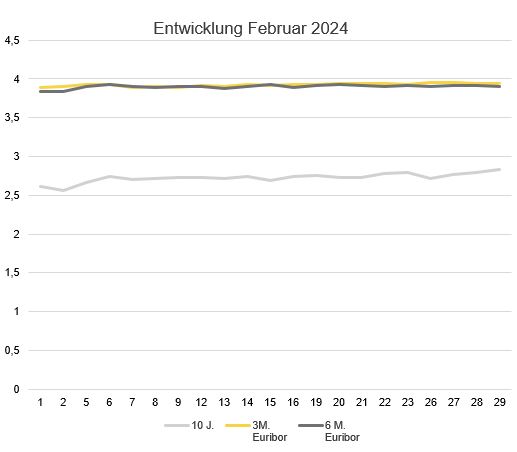

March has seen a lateral movement of interest rates emerge. Fluctuations remain as manageable as they were the previous month. Short-term interest rates have been particularly stable this month. The 3-month Euribor declined almost imperceptibly from 3.938 percent at the beginning of the month to 3.929 percent month-end. Similarly, the 6-month Euribor manifested a lateral trend, dropping from 3.912 percent at the beginning of the month to 3.905 percent in the course of the month. Only the long-term interest rates are visibly following a downtrend. For example, the 10-year interest rate swap declined from 2.74 percent at the start of the month down to 2.57 percent as the month progressed.

Outlook

The lingering challenges that the real estate market presents have prompted a shift in perspective within the industry. Over time, the majority of players have come to accept and adapt to the new interest rate levels and price corrections. While hopes persist that the ECB will cut its lending rates soon in response to declining consumer inflation rates, bank lending remains restrictive for the time being. Accordingly, further corporate insolvencies cannot be ruled out. Some companies have started seizing the emergent opportunities. Those who manage to adapt their strategies flexibly to the dynamic market environment, act swiftly and have the necessary equity on hand will emerge as the winners of the situation. Although MIPIM is primarily an industry meet, there might be more cause to celebrate at the next edition of the event a year from now. But not everyone will still be around by then.