Loading content …

Real Estate Prices Have Not Bottomed Out Yet

According to publications by the Association of German Mortgage Credit Banks (vdp), real estate prices in Germany have not bottomed out yet. While retail and office properties have been particularly hard hit, prices for residential real estate have also been softening. The office real estate market continues to face a contraction in demand, which in some cases has impacted the price level as well. But not just office real estate has felt the ramifications of the high level of inflation, as the retail sector is registering cutbacks as well. Private households have lost some of their purchasing power and therefore reduced their consumer spending. Since retail property rents tend to be tied to retail sales, rent rates have declined accordingly. At the same time, the increased level of interest rates has raised return requirements and therefore put pressure on prices.

Compared to the commercial real estate, price corrections on the residential property market are rather modest. In major German cities, prices for apartments and free-standing homes dropped by 1.4 percent within a year. The housing market in Frankfurt has been affected more than others. Year on year, it suffered a significant dip by almost 6 percent. The other major cities in Germany reported price corrections in a range between two and four percent. Only Berlin took exception to the trend. Since the housing market of the German capital continues to be severely strained, residential property prices here have remained largely stable so far. In fact, Berlin experienced price growth rates of around one percent year on year lately, unlike the other “Big 7” metropolises.

Due to the high level of interest rates and the rise in construction costs, the number of planning consents has dropped sharply. Yet in the absence of development projects, the demand for housing accommodation simply goes unmet. As a result, the situation remains strained in many housing markets, with rising rent rates the downstream consequence. These in turn are precisely what bolsters the high residential property prices. However, we are looking at a long-term process. In the short and medium term, the effects of the interest rate reversal are much more keenly felt. Unlike the major cities, regions with less strained housing markets, especially in economically underdeveloped parts of the country, are expected to see stronger price corrections.

Financing Conditions Hamper Transactions and New-Build Construction

Given the persistently high level of inflation, the situation cannot be expected to ease any time soon. The inflation rate predicted for the second half-year of 2023 is about 6 percent. The associated losses in popular prosperity will deepen proportionately. In the medium term, the consumer inflation rate is expected to stabilise somewhere between 3 and 4 percent. Interest rates should therefore not be expected to decline. In fact, the ECB has hinted at further, albeit modest, interest rate moves. The number of transactions and property developments is therefore on a historically low level. The few acquisitions and building projects that move ahead anyway stand out because of their distinct focus on sustainability. Compliance with ESG standards is fast becoming the key criterion in real estate financing. While the parameters may be less favourable, financing continues to be available for (residential) property development projects if the equity capital commitment is increased and the focus shifted to ESG requirements.

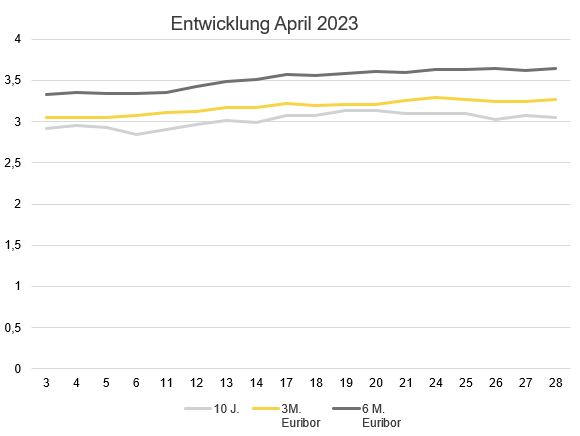

Interest Rate Development

Initially, long-term interest rates kept going up in April. But in early May, a slightly regressive trend in interest rates was in evidence. The 10-year interest rate swap rose from 2.92 percent at the start of April all the way up to 3.05 percent in the course of the month. The first half of May saw another modest recovery to 2.99 percent at the last count. Short term interest, by contrast, continued to climb. At the start of April 2023, the 3-month Euribor still stood at 3.05 percent. As the month progressed, the rate went up to 3.27 percent, and the upward trend continued into the month of May. Most recently, the 3-month Euribor crossed the mark of 3.30 percent.

Outlook

In the ongoing first half-year of 2023, the interest level continues to hold back transaction activities, and the cycle of price corrections has yet to be concluded. Inflation forecasts across the board predict a level above 2 percent. Accordingly, interest rates should not be expected to decline any time soon. But the options available to the ECB to fight inflation are limited. That said, it is precisely the current level of inflation that opens up investment opportunities, especially when fixed long-term interest rates come into play.