Loading content …

Moderate Long-Term Inflation Expectations

Despite an inflation rate of 7.9 percent in May and rising interest levels, the real estate industry has principally proven crisis-resistant. The interest rate development of 10-year German government bonds shows that long-term interest has reached a plateau, not least because the margin for interest-tightening remains limited.

The increase in construction costs and the elevated interest rates have put the industry as a whole under considerable pressure. A number of new-build construction projects have been shelved or put on halt. However, the construction cost growth appears to have peaked now. The prices for some materials have already started to drop – such as the price for timber. Principally speaking, the real estate industry has proven very crisis-resistant so far. Even sentiment among many market players has followed a positive trend, in spite of the difficult situation. Large transactions and financing arrangements continue to be negotiated, although it should be added that there is currently no evidence for any classic forward deals. Banks remain cautious, but not more so than they already were at the beginning of the year. All things considered, it is safe to say that the crisis is far from over.

Central Banks have Little Influence on Inflation

The rise in energy prices and shortage in raw materials keep fuelling the inflation and with it the long-term trend in interest rates. Central banks have few means to influence the situation. They would normally raise lending rates in order to address inflation, the idea being to dampen corporate investments and private consumption by increasing borrowing costs. However, the current inflation cycle is driven by short supply, which would be adversely affected by interest rate hikes, if anything.

It is hard to say at this point how central banks will respond to the situation in the long term. The Federal Reserve Bank has already raised its lending rates several times in a rather aggressive manner and announced further interest tightening moves, evidently willing to risk of an economic slump. By contrast, the European Central Bank has so far maintained its wait-and-see attitude. To be sure, it did announce an initial interest move for 21 July and will in all likelihood go through with it, too. But if the business cycle in Europe were to take a downturn, we consider it by all means possible that the ECB will revive its accommodative policy measures.

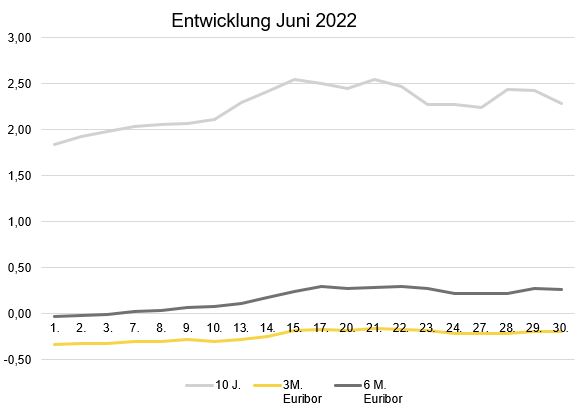

Interest Rate Development

Long-term interest rates rose in June. The 10-year interest rate swap increased from 1.84 percent at the beginning of the month to a month-end value of 2.28 percent. The increase for short-term interest rates was equally fast. The 3-month Euribor went up from -0.335 percent in early June to -0.195 percent at the last count. The 6-month Euribor also surged, from -0.334 percent at the beginning of the month to 0.263 percent by its end.

Outlook

Several scholars and leading chief economists expect the inflation to subside again in the medium term, and significantly so. Those reluctant to trust the science may check the so-called break-even inflation rate, meaning the difference between conventional German government bonds and their inflation-indexed equivalent. At the moment, the rate indicates that the inflation rate, while showing around 5 percent for the next twelve months, projects only 2.27 percent for the coming 8 years. This means investors are confident that the inflation will go back down again very soon, albeit much higher than the pre-Corona level. Hypothetically, the Euribor, and with it the short-term interest rates, will soon exceed the 2-percent mark. But it remains to be seen whether the ECB will actually implement its plan. For the time being, we consider this rather unlikely. We also believe that the Fed will lower its lending rates again once the impact on business cycle and labour market becomes too strong. Another factor to consider is that the high indebtedness of many eurozone member states would not tolerate a very high interest level. But the time for ultra-low lending rates has probably come and gone for good. Still, the low-interest cycle will be with us for a good long while yet.

Disclaimer:

The article reflect the opinion of the authors. Nevertheless, the provider and authors assume no liability for the accuracy, completeness and timeliness of the information provided. In particular, the information is of a general nature and does not constitute legally binding advice.

Publisher

Francesco Fedele Prof. Dr. Steffen Sebastian

Prof. Dr. Steffen Sebastian

Holder of the Chair of Real Estate Finance

at IREBS, University Regensburg

Francesco Fedele

CEO, BF.direkt AG