Loading content …

Financial Markets Show Calm Response to Iran Crisis

Massive upheavals on the financial markets were to be expected in the wake of the attack on Iran. There are fears that energy prices could go up, inflationary pressures increase and interest rates tighten as a result. But so far, the reaction of the financial markets has been surprisingly mild. For the time being, this implies stability for the real estate and construction sectors – if still on a heightened risk level.

The military assault on Iran has brought to mind the repercussions of the war in Ukraine and the oil price shocks of past decades. The ramifications to be expected now are obvious: rising energy prices, renewed inflationary pressures and, as a result, a possible increase in capital market rates. Rising energy prices would moreover raise concerns about another global economic dip and with it a return to stagflation.

So far, the actual reactions seen on financial markets have clearly been more sober. While oil prices and the volatility on the stock markets did increase as soon as this turn of events made the news, there has been no sustained flight movement away from risk assets.

Nor have the interest rate markets manifested any dramatic spikes. Capital market rates, especially the returns on German government bonds, have largely stayed within their current range. For the time being, market players evidently assume that the situation will not escalate beyond the region and not permanently disrupt global trade flows.

Unlike the situation during the pandemic, supply chains are far more robust and diversified today. Businesses have reduced their dependencies, adapted their inventories and tapped alternative sources for their commodities. From the present perspective, a repeat of the massive supply bottlenecks seen in 2020/2021 seems rather unlikely therefore. That being said, it cannot be ruled out either, least of all in the event of a prolonged military conflict.

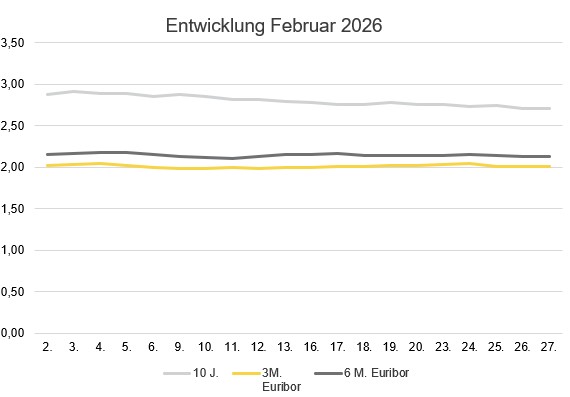

Interest Rate Development in February 2026

February 2026 saw borrowing rates go down slightly within a narrow range. The 3-month Euribor fell from around 2.03 percent in January to below 2.00 percent for a period of time before bouncing back to around 2.01 percent. The 6-month Euribor maintained a stable level between 2.13 and 2.16 percent.

On the long side, the 10-year swap rate was somewhat weaker than it had been the previous month. Having achieved rates of around 2,90 to 2.95 percent in January, it hovered between 2.70 and 2.80 percent in February. This means the run-up to the military intervention witnessed no crisis-induced interest rate movement either. Markets have priced in neither a rapid easing nor a renewed tightening of the monetary policy.

Ramifications for the Real Estate and Construction Sectors

As long as the conflict remains geographically and temporally confined, the ramifications for the real estate industry are likely to stay manageable. While rising energy prices could further drive up construction and operating costs, they would hardly trigger direct structural market upheavals. Lasting inflationary pressures that would further delay interest rate cuts and keep financing costs on a high level would pose a bigger problem. But there are currently not indications for these.

In fact, financial markets have so far shown a much calmer response than initially anticipated. Although this does not translate into an all-clear signal for the real estate industry, it does suggests a certain stability within an already demanding environment. The crucial aspect will be whether a geopolitical shock will prompt permanent inflationary pressures – or whether the impact will be limited to a temporary disruption. Everything will depend on the way in which financial markets develop in the coming weeks.